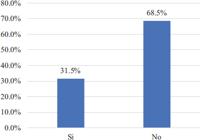

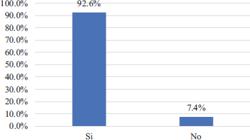

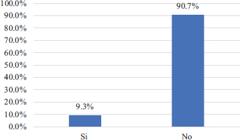

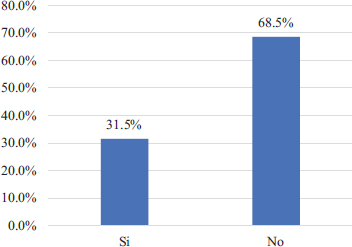

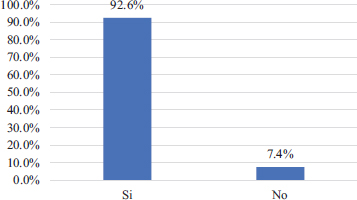

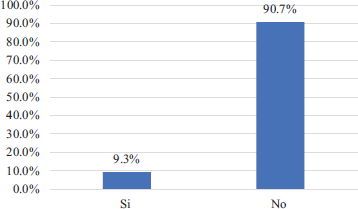

Introduction: The ethics of the public accountant, crucial for their profession, is based on regulations that support its application, with integrity standing out as an essential component. Objective: This study aims to characterize professional perceptions of ethics in tax auditing in Barranquilla, Colombia. Methodology: The research, with a quantitative, descriptive, and cross-sectional approach, employs a validated questionnaire applied to 54 public accountants acting as tax auditors. Results: Findings reveal that 68.5% lack specific ethical training, raising questions about ethical foundations. Nevertheless, 92.6% acknowledge the importance of ethics in tax auditing. Paradoxically, 90.7% perceive a lack of ethical importance in Barranquilla's companies, questioning the work environment. Academic training (59.3%) stands out as a key factor, and unanimous support for stricter codes of conduct reflects a general desire to strengthen ethical standards in the business sphere. Conclusion: A complex ethical scenario unfolds in tax auditing in Barranquilla, presenting challenges in ethical training but a solid intrinsic awareness, emphasizing the need to assess and enhance professional ethics in this context.

Keywords:

ethics; tax auditing; professional perceptions; academic training; codes of conduct

Thumbnail

Thumbnail

Thumbnail

Thumbnail

Thumbnail

Thumbnail

Fuente: elaboración propia.

Fuente: elaboración propia.

Fuente: elaboración propia.

Fuente: elaboración propia.

Fuente: elaboración propia.

Fuente: elaboración propia.